The Home Loan Process

Demystifying Home Loans

If you haven’t experienced it before, the home loan process can feel overwhelming, but I will help you stay informed throughout the process, from pre-approval to closing. The first thing to do is consult with a mortgage specialist (or two). If you don’t already have someone in mind, I partner with some of the best lenders in the industry, and am happy to introduce you, so you’ll be taken care of.

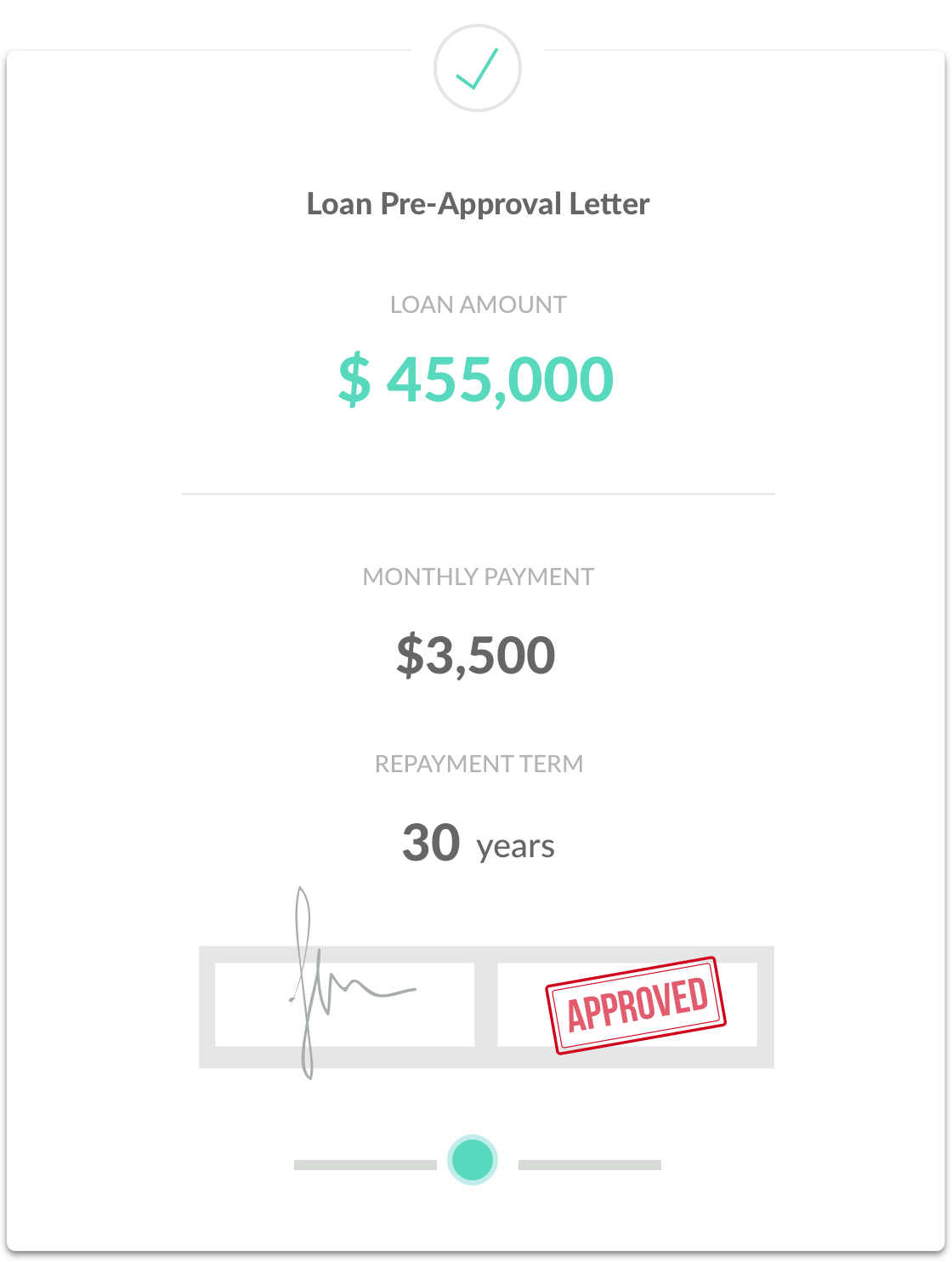

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Loan Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

Finance With

Academy Mortgage Corporation

Lori Meaney

Sales Manager, Producing

NMLS #1132235

- (352) 304-3747

- lori.meaney@academymortgage.com

- 5744 NE 61st Court 545, Silver Springs, FL 34488

Born and raised in Marion County, FL, Lori has been in the mortgage industry for over 26 years and is great with experienced or first-time home buyers as well as seasoned buyers. Lori can do VA, Conventional, USDA, and FHA as well as construction and down payment assistance loans. Lori explains the different loan options thoroughly so you can choose the best mortgage program for your specific needs. Whether purchasing or refinancing, Lori and her team will keep you informed and on track with your home buying process. She understands that there is no purchase more important, rewarding or exciting, as a new home. Your time is important and we understand that. With appraisers familiar with home values in your community, coupled with our “in-house” underwriting, funding and closing, our goal is to close on time, every time. Complete an online application, call, or email Lori today to make your dream of owning a home a reality!

I am licensed in: FL, GA #1132235, TN #1132235

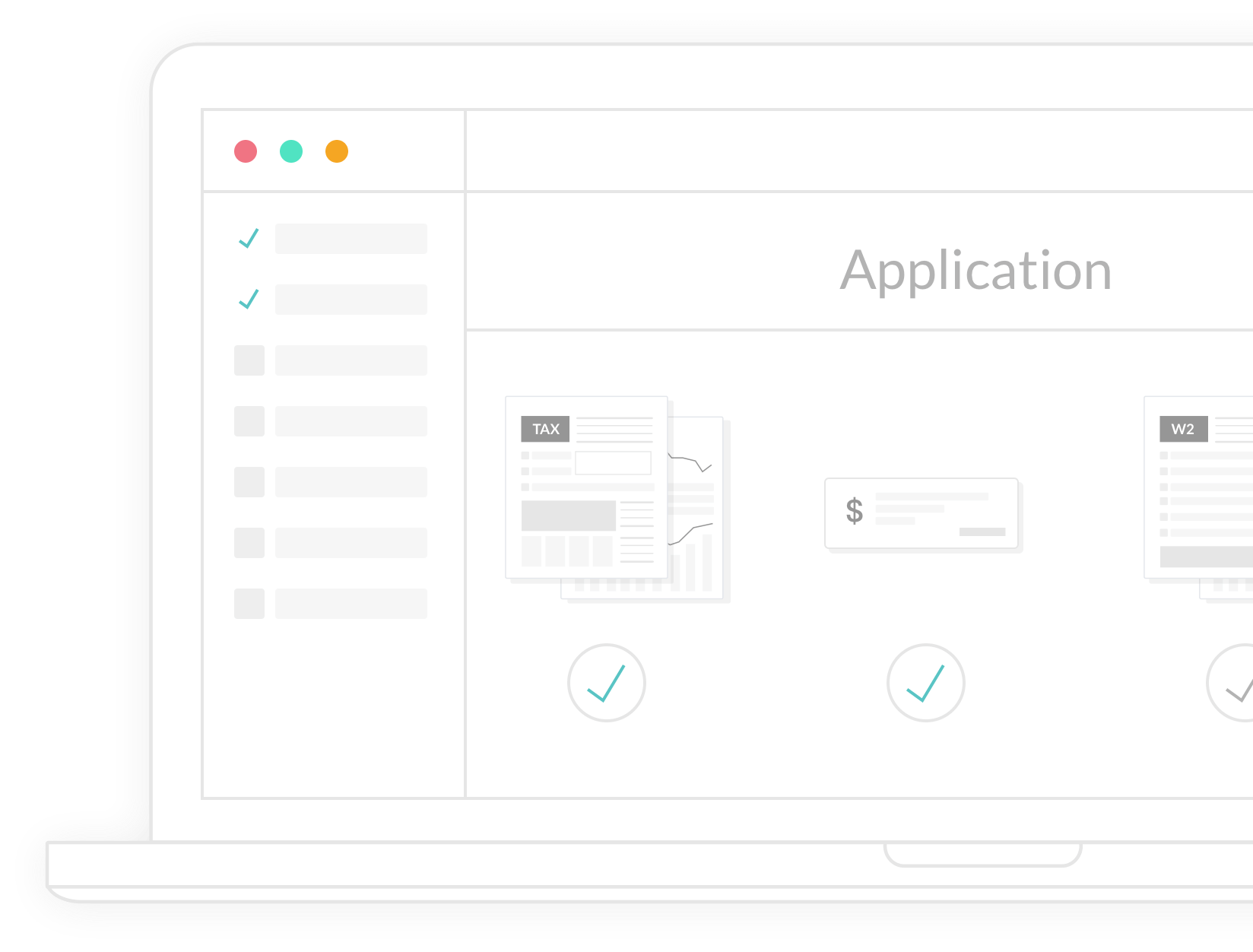

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!